Congratulations! You have worked hard all your life, made plenty of sacrifices, and you finally retire! But your investor’s life doesn’t stop here, it doesn’t “retire”. You now enter a new phase of portfolio management at retirement.

The idea now is to protect your capital. The trick is to make sure you have enough to continue enjoying your retirement. If you are very wealthy and don’t need much to live happily, bonds could work and do both (protection and income generation).

If you aspire to generate over 4% from your portfolio (which is reasonable), staying invested will be the preferred course of action. Here are three stock ideas that would fit well in a retirement portfolio.

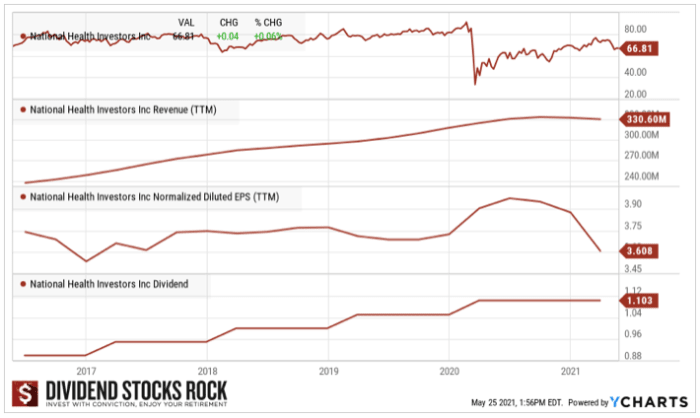

National Health Investors (NHI) 6.60% Yield

NHI is a high-quality healthcare REIT that owns a diversified property portfolio in over 30 U.S. states. Its cash flows are safe and regular as its tenants are engaged in providing healthcare services and senior living assistance to a large and aging generation. Management is optimistic for the future and expects volatility but not deterioration of its tenants’ credit. Many COVID-19 cases could hurt the NHI business model. So far, so good however as the REIT has collected 94.3% of its rent as of March 2021. There is an opportunity here but proceed with caution.

Source: December 2020 Investors Presentation

Potential Risks

Senior living facilities are expensive, and many people may prefer other options. Should this become a stronger trend, it could have a major impact. Plus, changing medical policies and rising labor costs are other potential risks. Medicare and Medicaid rates might also be affected by the recent tax reform. Medicare changes in 2000 led the REIT to cut its dividend. Still, demand could improve absorption rates. Finally, NHI has been on heavy watch since the pandemic hit the U.S. As the virus spreads, we don’t know how it will evolve within the NHI facilities. Risks have been controlled so far, but an outbreak could have devastating consequences. For example, NHI is in discussion with Bickford regarding additional rent deferrals (representing rent deferrals of 11% of all rent due in April) because of the ongoing impact from the pandemic.

Dividend Growth Perspective

NHI Dividend Profile

NHI is sharing strong dividend growth with shareholders, while reducing its AFFO payout ratio. The company has paid a dividend for more than 15 consecutive years. NHI shows a 6%+ CAGR dividend growth over the past 5 years, which is a lot better than many other REITs. With a reasonable payout, the REIT has enough room for future payout growth. We expect NHI to slow down its dividend growth pace while the virus persists. The AFFO payout ratio is at 82% (Q3 2020) which allows management adequate flexibility going forward.

Latest Quarter Update

It was a difficult quarter for NHI as it missed FFO expectations (down 9%). The decline in Net Operating Income is attributable to a $21 million gain on the sale of real estate assets in the first quarter of 2020, $4.2 million in rent deferrals incurred during the first quarter of 2021, and a $3.6 million year-over-year increase in non-cash stock-based compensation. As previously announced, NHI entered into a rent deferral agreement with Bickford which includes a deferral of $3.0 million for April and a deferral of $2.0 million for May. The dividend remains safe with a FFO payout ratio of 90%.

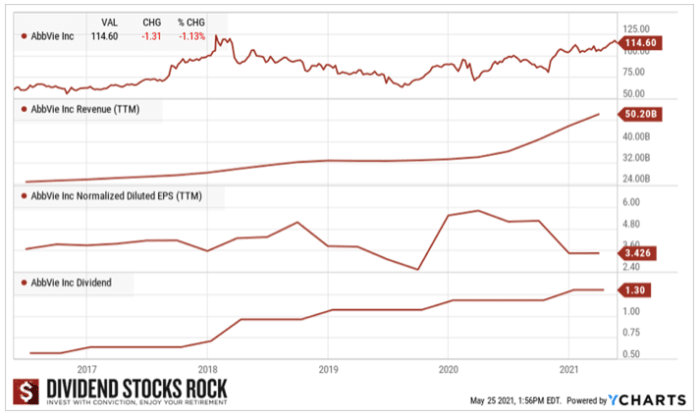

AbbVie (ABBV) 4.50% Yield

ABBV’s strength resides in Humira, a tumor necrosis factor blocker that reduces the effects of an inflammatory body substance. Humira is about 50% of ABBV sales and even more of its profit. The company is currently enjoying the last few years of Humira’s various patents across the world. New immunology drugs such as Skyrizi and Rinvoq could replace a good part of Humira’s sales slowdown. ABBV’s growth also lies in its new cancer drug, Imbruvica. We also see promising growth from its psoriasis and rheumatoid arthritis drugs. The idea behind buying Allergan was primarily to diversify ABBV revenue sources and find cleverer ways to extend its patents. AGN’s, like ABBV’s, legal department is known for its “creativity.” Issuing a trademark for Botox was very smart. The recent dividend increase confirms our bullish thesis.

Source: J.P. Morgan Healthcare Conference Presentation

Potential Risks

As the drama about Humira’s patent expiration (2023 for the U.S.) shows us, the drug industry is all about patents and competition. Why? Because it allows the winner to reap the benefits of billions invested in R&D. Therefore, ABBV must deal with competitors’ drugs not related to patents. While ABBV might be one discovery away from making billions, the same goes for about any competitor. For instance, Pfizer could deteriorate ABBV sales expectations. Now, ABBV must convince the market its pipeline is worthy of their investment. A few more quarters should be necessary. ABBV is increasing its leverage through the acquisition of Allergan. Both Humira from AbbVie and Botox from Allergan are star products that could face heavy competition going forward and hurt the ABBV bottom line.

Dividend Growth Perspective

ABBV Dividend Profile

ABBV has been quite generous with its shareholders lately. The company has successfully increased its dividend since 1973 (including Abbott’s history). Management has more than doubled its payout in the past 5 years on top of buying back shares. With a yield of 4.5%, it is a great candidate for any retirement portfolio. The company’s cash payout ratio is under control and high single-digit dividend raises should be maintained for a few more years.

Latest Quarter Update

ABBV beat both EPS and revenue growth expectations. Humira has been one of the growth drivers for AbbVie in recent years, but is set to face a patent cliff in the United States. U.S. Humira net revenues were $3.907B, an increase of 6.9%. Internationally, Humira net revenues were $960M, a decrease of 8.3%. While total revenue jumped by 51%, comparable revenue growth was 5.2% (excluding Allergan acquisition). Speaking of Allergan, global Botox Cosmetic net revenues were $477M, an increase of 44.7% on a comparable operational basis. Management raised 2021 Adjusted Diluted EPS Guidance Range from $12.32 to $12.52 to $12.37 to $12.57.

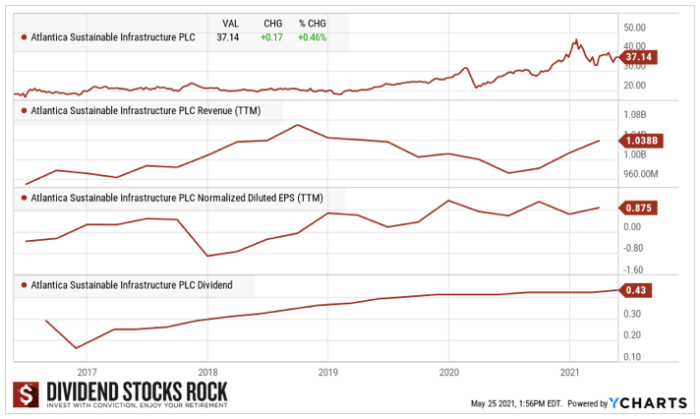

Atlantica Sustainable Infrastructure PLC (AY) 4.60% Yield

Atlantica is an interesting play in the sustainable energy world. 100% of its revenues come from assets with contracted PPA (power purchase agreements). AY enjoys long-term contracts (average of 18 years) with governments across the world to provide clean energy. We also like their geographic diversification. As it counts on predictable cash flow coming from its 100% regulated contracts, AY has developed a strong expertise in growth by acquisitions. If you like AY and don’t want to deal with the hassles of having a PLC in your portfolio, you can go with Algonquin Power (AQN.TO / AQN) as it owns 44% of the AY shares.

Potential Risks

While all looks pink with unicorns and rainbows, you must know Atlantica Yield had its fair share of trouble a few years ago. AY is a Yieldco. Yieldcos have a sponsor who develops and initially operates assets tied to long-term contracts. Then, the sponsor drops their assets into the Yieldcos and lets the company operate the assets in exchange for a juicy distribution. Back in 2017, AY’s former sponsor Abengoa sold its take in AY leaving the Yieldco alone. This is when Algonquin Power acquired 25% of the company (it currently owns a 44% interest). If you have a headache already, Yieldcos are not for you.

Dividend Growth Perspective

AY Dividend Profile

Atlantica has successfully increased its dividend annually since 2017. If you want to assess AY’s ability to pay dividends, you must look at their cash available for distribution (CAFD) payout ratio. The company currently sits on ample liquidity and has no major debt maturities until 2025. This leaves plenty of time and money to keep-up its dividend growth policy. Please note that AY is a PLC based in the UK. Verify the tax implications of withholding taxes, return of capital affecting cost basis, etc. The answers to those queries will guide you in which type of account you hold this investment in.

Latest Quarter Update

Recently, AY disappointed the market by missing both EPS and revenue growth. Revenue increase (+12%) was supported by the contribution of new assets, foreign exchange differences and higher solar resource and production in some assets. Production in the renewable energy portfolio increased by 15.2% for the first quarter of 2021 compared with the first quarter of 2020 mainly thanks to the contribution of the recent investments in solar assets and higher solar radiation and production in some assets. AY increased its dividend by another $0.01/share, congratulations!

Final Idea: Canadian Banks?

It’s not because I’m Canadian, but I must admit Canadian banks are unique. The Big Six operate an oligopoly that is not only highly regulated, but also is protected by the Canadian Government. In other words, they can use their core business in Canada to generate significant cash flows and use this money to grow outside those boundaries. This is how they can pay a yield around 3-4% and still show a 5% to 8% annualized dividend growth rate over decades. Dividends are paused due to the pandemic but will resume shortly after once this is under control. Even if you are American and must consider tax implications and currency fluctuation impacts, taking a look at these beauties wouldn’t hurt, especially since 5 of them trades on the NYSE:

- Royal Bank (RY) 3.62% yield

- TD Bank (TD) 3.87% yield

- ScotiaBank (BNS) 4.56% yield

- BMO (BMO) 3.77% yield

- CIBC (CM) 4.72% yield

- National Bank (NTIOF) 3.31% yield

Cheers,

Mike Heroux, Passionate Investor & founder of Dividend Stocks Rock

P.S. On a side note, I’ll hosted a free webinar about retirement and the withdrawal mechanics and you can watch the free replay here.

Follow me on