It’s exceptional to see a high-top quality, increasing, blue-chip healthcare share tumble 26%, but that is just what transpired to Resmed CDI (ASX: RMD) following its Q4 2023 financial success.

ResMed is a globe chief in gadgets and know-how for the therapy of sleep apnea. It sells merchandise and computer software to buyers all about the world. It has finished for several years…

So is ResMed’s share value an allergic reaction to Ozempic, or a little something else?

Is ResMed fundamentally weakened?

Or does this present the best getting chance for ResMed shares because 2017?

Let us dive in…

ResMed share selling price

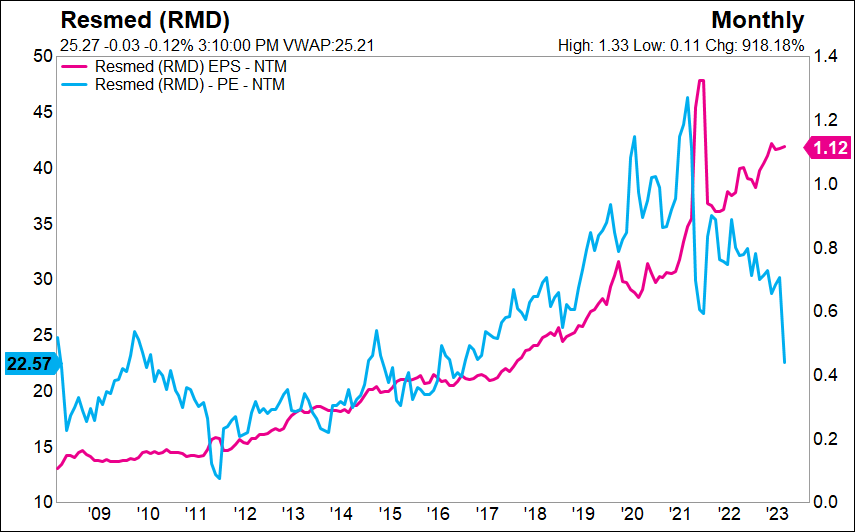

ResMed produced A$.98 of earnings for every share in FY23, up from $.82 in FY22, and is forecast to mature even further in FY24, to $1.09 for every share, so what is bought the industry spooked?

ResMed’s declining margins

In Q4’23, ResMed described gross margins of 55.8% (down -2.05% calendar year-on-12 months) which was .65% down below analyst consensus estimates. Not ordinarily a signal of a business enterprise with significant pricing electric power or a defendable moat.

On the other hand, digging in a small more we see that Resmed’s Product profits grew +24% in constant currency conditions, a lot quicker than Masks revenue which grew +18%. As Products are a drastically reduced margin products than Masks, this sales expansion mix negatively impacted gross margins.

Accelerating Product profits have been a predictor of foreseeable future accelerating mask revenue, so we assume these margins normalise above time.

At an running stage, declining freight, labour and devices charges should really also aid increase ResMed’s foreseeable future revenue margins. We feel the company’s effort to simplify its product or service suite and optimise its output line should also not be underestimated in its skill to push profitability larger.

Some argue that ResMed’s Mask company will be completely impacted by raising opposition, notably from Phillips. We consider this argument is flawed, significantly provided the reputational destruction experienced by Phillips just after its product remember 2 yrs in the past.

In 2020, prior to the recall, Phillips was targeting €700-800m in mask sales by CY25. That focus on has been lowered to only €400m in product sales and in its most modern Q2 success, Phillips observed income declining in its sleep and respiratory treatment division as it carries on to shed sector share to ResMed.

The industry appears to be to believe this reputational harm to Phillips will only profit ResMed for a single yr. Nevertheless, it appears to be to be nevertheless successful industry share two several years on, and we imagine its instructive to study the influence of a item recall at ASX-outlined health care peer Cochlear Restricted (ASX: COH), which misplaced marketplace share for 8 many years after its solution recall.

It is fair to say that people really do not like to just take any possible chance when it will come to their overall health.

Ozempic

Novo Nordisk A/S’s (CPH: NOVO-B) pill is an oral edition of semaglutide, the active ingredient in the company’s blockbuster fat reduction injections Ozempic and Wegovy (which the organization has struggled to hold up output for, thanks to the extremely significant desire).

Semaglutide mimics a hormone created in the intestine termed GLP-1, which indicators to the brain when a person is total. A late-stage trial in June 2023 discovered that a higher dosage of the drug assisted overweight older people lose 15% of their human body body weight. The after-a-working day tablet does have some side results, typically mild-to-reasonable nausea, constipation, diarrhea, and vomiting.

This is all appropriate to ResMed as sleep apnea has until finally not long ago primarily been diagnosed in middle-aged overweight men. Nonetheless, management are speedy to place out (in the new once-a-year report) that approximately 40% of new CPAP people are woman.

In any circumstance, is this ‘wonder drug’ the heal for obesity and as a consequence, sleep apnea?

We assume not.

Though obese individuals usually have sleep apnea, not all sleep apnea sufferers are obese. People today with hypertension (83%), continual heart failure (76%) and form-2 diabetes (72%) all put up with from large instance of slumber apnoea.

As a result, the sleep apnea addressable industry is enormous, approximated to be roughly 900 million people today globally and with only 16 million men and women on CPAP products, and with 80% of individuals undiagnosed, this extremely huge marketplace stays underpenetrated.

The upshot here is there is enough scope for both equally Ozempic and sleep apnea to co-exist and certainly for ResMed to continue on its double-digit organic advancement runway.

What is the upside for the RMD share selling price?

At $25.00 for each share, we feel the industry is now underappreciating a business that can sustainably make >15% best line expansion, at 30% EBITDA margins and 20% return on invested cash (ROIC) from mainly recurring revenues.

On that foundation, in 3 many years ResMed will be making $1.7bn in web income. Assuming it trades on the exact 30x selling price-earnings ratio (P/E) it traded at pre-benefits, the inventory is really worth ~$35 per share prior to buybacks or other cash administration.

In higher high quality, substantial cap businesses, these sorts of chances only flip up after in a blue moon – ordinarily when there is a prevailing, exaggerated and feared change in narrative.

In our perspective, narratives are most effective left for bedtime and traders ought to concentrate on the knowledge.